Digging Into the Data to Uncover School District Fraud

Forensics & Litigation Services

Forensics & Litigation Services

Never miss a thing.

Sign up to receive our insights newsletter.

Like archaeologists using geothermal tools to pinpoint digging locations, forensic investigators have discovered how to use data analytics to help school districts narrow in on potential fraud, waste and abuse. By examining expenditures in more granular cost categories and comparing the data to other districts, we can create heat maps that help us identify potential red flags, including fraud schemes like vendor kickbacks that are difficult to detect using traditional approaches.

An Information Treasure Trove for School Districts

With standardized financial data collected annually for over 1,200 school districts and charter schools in Texas, TEA’s Public Education Information Management System (PEIMS) provides a treasure trove for data analytics. By conducting external benchmarking and applying data analytics to the PEIMS data, we can identify specific cost categories where a school district may be paying more for services, supplies or equipment compared to their peers, potentially warranting further review or investigation.

Getting Granular

Financial activity for school districts is primarily reported at the “Function” level in the audited financial statements (Instruction, Health Services, etc.). For our purposes, however, these categories (typically less than 20) are often too broad to identify and detect red flags. We need to dig deeper.

Fortunately, PEIMS data is structured to also include more than 75 Object codes that provide more detail about the nature of the expenditure (e.g., consulting services or miscellaneous operating costs). Using both Function and Object codes, we can analyze the data in more than 1,200 cost categories. Looking at the information at this granular level allows us to make observations and identify anomalies that would be difficult to detect when only analyzing the Function level data.

External Benchmarking

The standardization of expenditure coding and classification in the PEIMS data across Function and Object codes also allows us to compare the same expenditures with other school districts on an apples–to- apples basis. We can normalize the data by analyzing expenditures within each cost category on a per student basis to account for size differences between school districts.

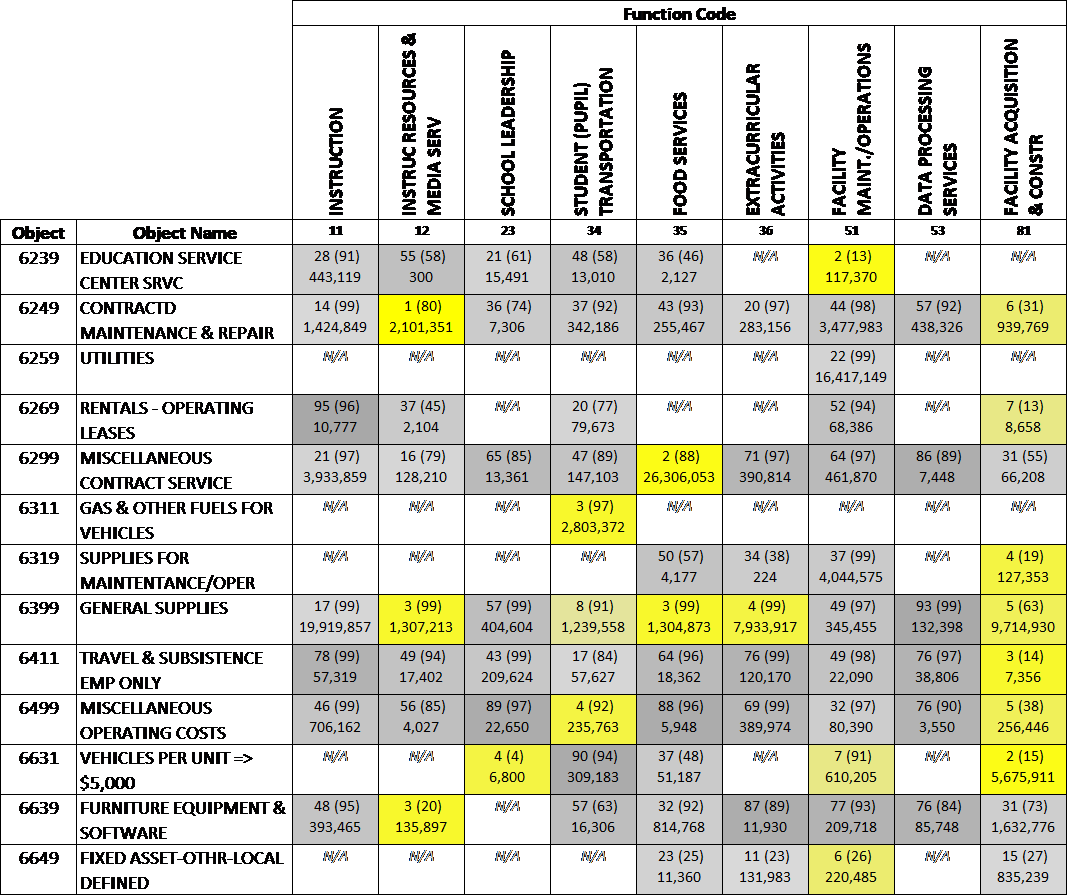

The heat map in the example below incorporates data analytics to examine a school district’s expenditures over a three-year period, with a matrix structure to reflect cost categories defined by Function and Object codes, and incorporating external benchmarking data. For each cost category (i.e., grid cell), the top set of numbers represents the school district’s ranking compared to a defined peer group (i.e., 28th out of 91), with the bottom number showing the total expenditures for the cost category for the three-year period. Potential red flags, highlighted in yellow, identify cost categories where a district’s expenditures are anomalously high in comparison to other districts. There may be valid reasons for these anomalies, but these are areas an internal auditor or fraud investigator would want to examine further to understand the root cause.

Because of the volume of expenses associated with school district operations, time and resource constraints alone require us to be selective in identifying areas for digging deeper. Data analytics allow us to narrow the focus and identify any higher risk cost categories that should be monitored or examined more closely.

Historically, the most common way for school districts to detect fraud has been through tips, with knowledgeable employees coming forward with information regarding the alleged impropriety. Incorporating data analytics can enhance a district’s fraud risk program by providing a powerful tool to proactively monitor and detect higher risk cost categories for fraud, waste and abuse.

For more information, contact us. We’re here to help.

© 2022