The Outpatient Joint Replacement Boom May Be Reaching Its Peak

Health Care Valuation Services

Health Care Valuation Services

Never miss a thing.

Sign up to receive our insights newsletter.

Health Care Valuation Implications

The decade-long migration of total joint procedures from hospitals to ambulatory surgery centers (ASCs) may be approaching a structural ceiling. Total joint replacement, including hip and knee arthroplasty, is one of the highest-volume elective surgical categories in the U.S. and a significant revenue driver for both hospitals and ASCs. The site of care for these procedures has significant financial implications for health systems, payers and ASCs.

Since the Centers for Medicare & Medicaid Services (CMS) removed total knee and hip replacements from its inpatient-only list, structural tailwinds supporting the shift of these cases to the outpatient setting remain robust. ASCs are typically lower cost, popular with patients and preferred by payers. However, the patient population that was ideally suited for outpatient joint replacement — younger, healthier, lower body mass index (BMI) patients — has largely been captured, which may limit the pace of further migration.

By the Numbers

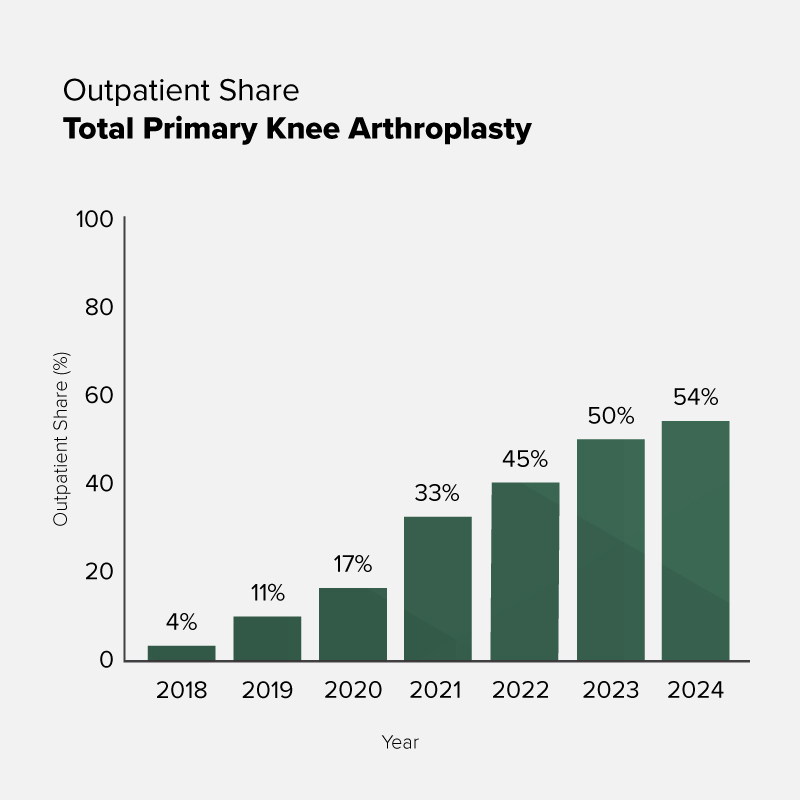

Outpatient share of primary total knee surgeries reached 54% in 2024, up from under 5% in 2018. Yet, growth has materially decelerated since 2022, with single-digit annual share gains replacing the 8-12 point leaps of the post CMS rule era, signaling a shift from rapid expansion to more moderate growth.

Source: CMS claims data, industry analyst estimates

Outpatient share of total primary knee arthroplasty increased steadily after 2018, with 7% growth rates in 2019 and 2020. Growth accelerated to 16% in 2021 and 12% in 2022, before slowing to 5% and 4% in 2023 and 2024, respectively, further indicating that the steepest gains in outpatient migration may have already occurred.

The Forces Slowing Growth

Patient complexity

A meaningful portion of the inpatient joint volume is correlated with cases that are less suitable for outpatient discharge, including those with obesity, diabetes, cardiovascular conditions or social barriers to home recovery. These cases will likely remain in the inpatient setting, creating a practical floor for hospital-based volumes.

Revision surgery

Total joint revisions — which are growing as the installed base of primary procedures ages — remain overwhelmingly hospital-based. As the revision mix grows relative to primaries, it shifts the overall case volume back toward inpatient settings.

Surgeon alignment

Alignment between surgeons and sites of care has matured. Many of the ASC-friendly orthopedic surgeons have already migrated their patient volume to the ASC in recent years. Some total joint surgeons are now employed by health systems, ensuring that the corresponding surgery volume will remain in the hospital.

Health Care Valuation Takeaways

- Valuators should be cautious when evaluating projections that assume continued growth of total joint procedures to ASCs. Volumes will remain healthy, but year-over-year growth may slow, affecting valuation multiples for ASC platforms.

- The most accessible outpatient migration may have already occurred. Future growth will be more limited, as the remaining total joint volume, often for valid clinical reasons, may stay in the hospital, making future gains more incremental rather than structural.

- Hospitals, even systems that are part owners in ASCs benefiting from migration, will use multiple competitive methods to retain total joint volume where they capture 100% of revenue and profits while maintaining patient relationships. The remaining hospital-aligned surgeons have economic, cultural and contractual reasons to continue to perform cases in the hospital.

- Valuators should consider incorporating an additional industry-specific risk factor into assumed ASC total joint volume growth. This adjustment better reflects the transition from rapid migration to a more mature, slower-growth environment.

What does the shift in outpatient joint migration mean for your health care organization’s strategy or valuation assumptions? Weaver can help assess how site-of-care trends may impact your forecasts, transactions and long-term planning. Contact us.

©2026