The Power Behind a Segmented Income Statement

For lenders or other outsiders, a companywide income statement may be enough to evaluate your company’s financial performance. However, from management’s perspective, a “segmented” income statement can provide valuable insight into key performance drivers and possible improvement strategies.

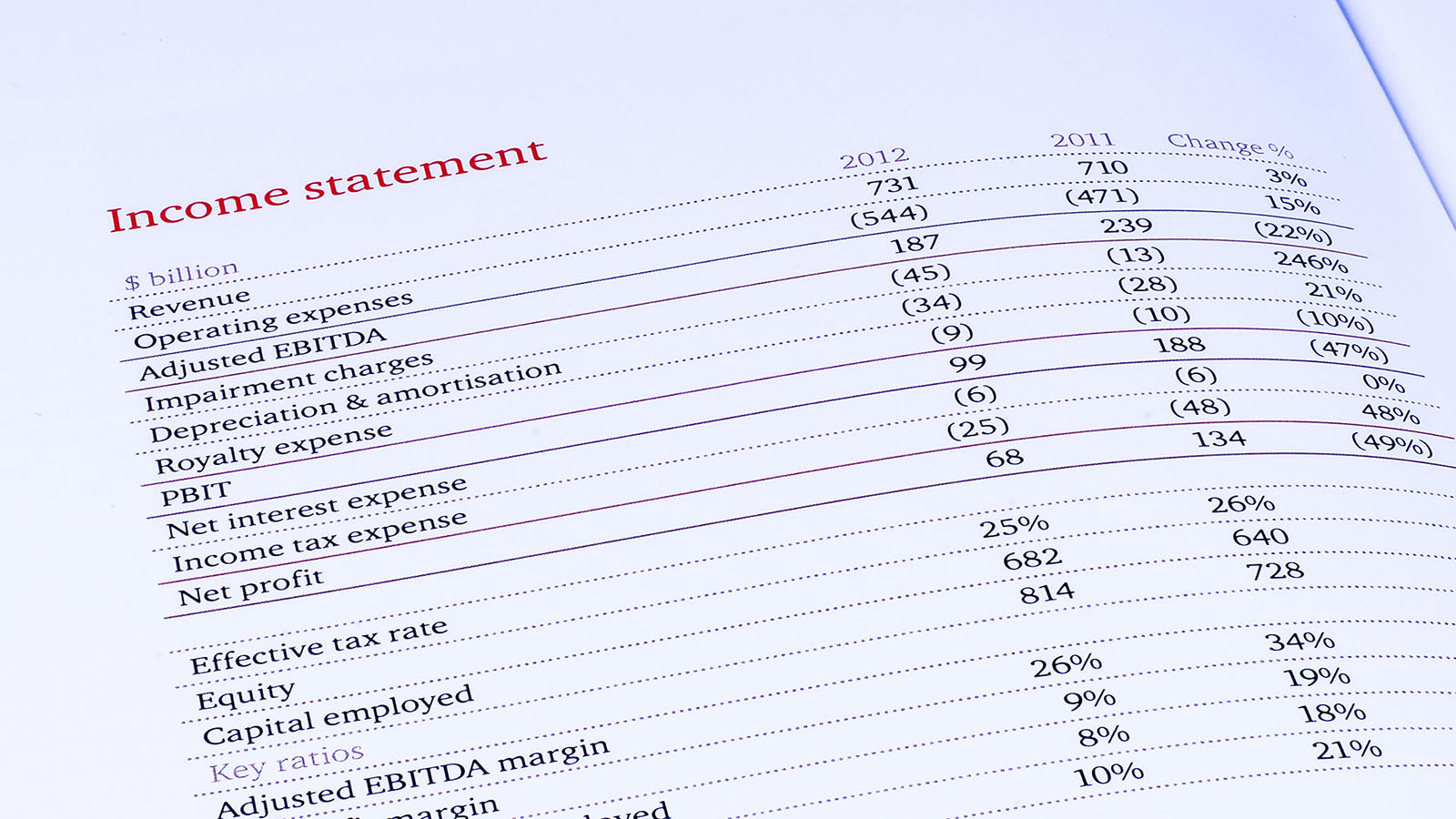

Segmented vs Traditional Income Statement

To arrive at a net profit or loss, a conventional income statement starts with revenue, and then subtracts costs. A segmented income statement provides additional detail via breaking down revenues and expenses by business unit, such as product line, location, department, salesperson or territory. This breakdown helps management identify underperforming segments and develop strategies for boosting profits.

Creating a segmented income statement can be challenging because you must assign costs to various segments. In addition to attributable direct costs, such as materials and direct labor, you’ll need to allocate a portion of the company’s indirect costs, such as rent, insurance, utilities and executive salaries, to each segment.

The extent to which a segment benefits from or drives costs determines how indirect costs are allocated. For example, you might allocate indirect costs based on segments’ relative sales dollars, units sold, direct labor hours or floor space occupied. Different methods may produce different results, so select a method carefully to ensure it fairly reflects each segment’s net income.

Are Your Segments Worth Retaining?

If you uncover underperforming business units, segmented income statements can help remedy the situation. Depending on the reasons for a segment’s poor performance, potential strategies might include:

- Increasing prices

- Reducing costs

- Addressing quality or design issues

- Shutting down a segment

If a segment is operating at a loss, closing it doesn’t necessarily mean that it will benefit the company. Terminating an underperforming segment, in some cases, can cause the company’s overall net income to go down. How’s that possible? Because a seemingly unprofitable segment may still contribute to the company’s net income.

Most indirect expenses allocated to a segment, as well as some direct expenses, are fixed. This means that your company will continue to incur them, even if you eliminate the segment. Therefore, you may be better off retaining a segment if it contributes to companywide net income, even if it is operating at a loss.

Calculate the contribution margin — which is simply revenue less variable costs — to determine whether a segment is making a contribution. Variable costs are those that increase or decrease with the level of production output and, therefore, will drop to zero if a segment is shut down.

It is probably worth keeping a segment that has a positive contribution margin, and is adding revenue to the company’s fixed costs and profit. So, it’s a good idea to report contribution margins on your segmented income statement.

Let Us Help

If properly designed, a segmented income statement can enhance profitability. It is important to remember that when determining an appropriate method for allocating costs amount segments, it requires significant professional judgment. For assistance, consult one of our Weaver professionals today.

© 2020