The Federal Reserve's Main Street Lending Program Overview and Guidance

Overview:

The Main Street Lending Program (MSLP or Program) is designed to support small and medium-sized businesses and help them recover from the adverse impact of COVID-19. On June 8, 2020, Program eligibility was expanded by the Federal Reserve (Fed) so more businesses can participate and receive financial support. The availability of additional credit will help companies that were in sound financial condition prior to the onset of the pandemic maintain their operations and payroll until conditions normalize.

As cited in the June 8th MSLP FAQs, the changes to the Program include:

- Lowering the minimum loan size for certain loans from $500,000 to $250,000

- Increasing the maximum loan size for all facilities (see chart below for new loan sizes)

- Increasing the term of each loan option from four years to five years

- Extending the repayment period for principal for all loans from one year to two years

- Raising the Reserve Bank’s participation to 95% for all loans

Main Street Loan Applications

Borrowers can receive a Program loan from any eligible lender. The lender process will be similar to the Paycheck Protection Program (PPP) where U.S. insured depository institutions, U.S. bank holding companies and U.S. savings and loan holding companies will be offering the loans.

Once borrowers have successfully registered for the MSLP, lenders are encouraged to begin making Main Street loans immediately provided the required documentation is complete and the transactions are consistent with the credit facility’s requirements. The Program will also accept loans that were originated under the previously announced MSLP terms, if funded before June 10, 2020.

The MSLP Credit Facilities

The Program will be implemented by the Federal Reserve Bank of Boston (FRB Boston). FRB Boston will set up a special purpose vehicle, Main Street SPV, to purchase participations of 95% of the loans originated. Eligible lenders will retain the remaining 5%.

The MSLP will operate through three loan facilities:

- The Main Street New Loan Facility (MSNLF)

- The Main Street Priority Loan Facility (MSPLF)

- The Main Street Expanded Loan Facility (MSELF)

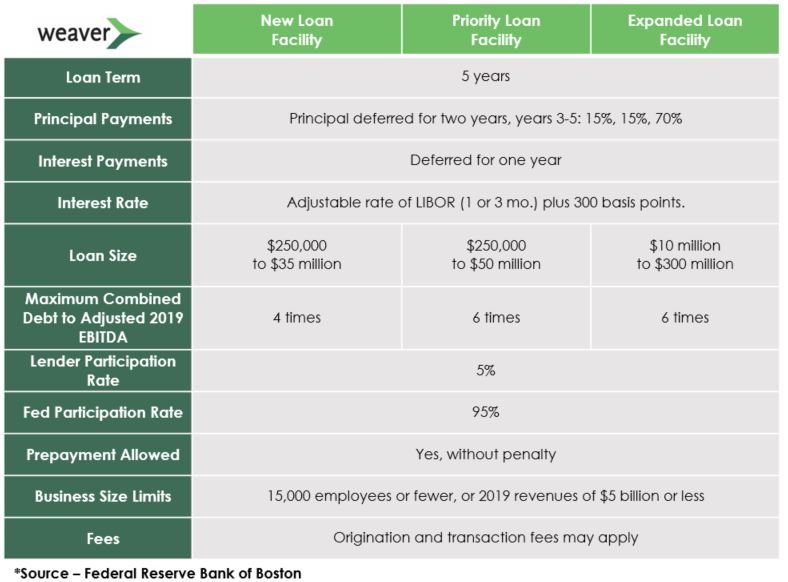

Loans have a five-year maturity, deferral of principal payments for two years, and deferral of interest payments for one year. Depending on your existing debt and liquidity needs, eligible lenders will recommend and originate the new loans (under MSNLF and MSPLF) or increase the size of (or “upsize”) existing loans (under MSELF). All three facilities use the same eligible lender and eligible borrower criteria.

MSLP Eligibility Criteria for Borrowers

A business that meets the following criteria is eligible for the Program:

- Was established prior to March 13, 2020

- Is not an ineligible business under SBA regulations for purposes of the PPP

- Meets at least one of the following two conditions:

- Has 15,000 employees or fewer, or

- Has 2019 annual revenues of $5 billion or less

- Is organized in the U.S. or under U.S. law with significant operations and a majority of its employees based in the U.S.

- Only participates in one of the Main Street facilities (MSNLF, MSPLF or MSELF). They must also not be a participant in the Fed’s Primary Market Corporate Credit Facility (PMCCF), or has not received specific support from other CARES Act provisions

- Is able to make all of the certifications and covenants required under the MSLP

Differences between the PPP, the MSLP and the PMCCF

Similar to the PPP and the PMCCF, the Program was created to assist companies that have been adversely affected by COVID-19. Each program was developed to provide liquidity to companies of different sizes and/or with different needs:

- PPP: Established by the SBA to support the payroll and operations of small businesses with government-guaranteed loans that include a forgiveness feature.

- MSLP: Supports small and medium-sized businesses unable to access the PPP or that require additional financial support after receiving a PPP loan. Loans are not forgivable.

- PMCCF: Supports large businesses by providing access to credit for new bond and loan issuances. PMCCF loans are not forgivable.

Businesses that received a PPP or Economic Injury Disaster Loan (EIDL) are eligible under the MSLP if they meet the eligible borrower criteria.

MSLP Effective Date

The Program has been established to respond to uncertainty related to COVID-19, and borrowers can participate in the three loan facilities through September 30, 2020. The Main Street SPV will cease purchasing loan participations on September 30, 2020, unless the Program is extended by the Fed and Treasury Department. FRB Boston will continue to operate the Main Street SPV until the assets mature or are sold.

Outstanding PPP Loans

Any PPP loan balance that has not yet been forgiven is counted as outstanding debt for the purposes of the MSLP maximum loan size test.

Eligibility of Not-for-Profit Organizations

While not-for-profits are not currently eligible, the Fed announced on June 8, 2020 that it is working to establish one or more loan options suitable for not-for-profit organizations.

The Lender’s Role in Verifying Certifications and Covenants

Lenders are required to collect certifications from borrowers at origination or upsizing and may rely on the information as well as subsequent self-reporting by the borrower. Lenders are not expected to independently verify the borrower’s certifications or monitor ongoing compliance with covenants. If lenders become aware of a material misstatement or breach in covenant during the term, they are to notify the FRB Boston.

Comparison of the Three Credit Facilities

Terms of the three credit facilities are compared in the chart below*:

The Fed also updated its FAQs on June 8, 2020 to provide more clarification and guidance.

How Weaver can help

Applying for and maintaining compliance with debt covenants and reporting requirements can be burdensome. Weaver can assist both borrowers and lenders in many different ways:

- Preparing and organizing borrower and lender documentation

- Developing cash flow models for loan payback consideration

- Evaluating restructuring options that consider existing debt and other obligations

- Developing tools to help monitor covenant compliance and ongoing reporting requirements

We welcome you to contact us for more information on lending programs, operational guidance, tax considerations, regulatory updates, IT best practices, and more.

© 2020