More Data! How to Meet Demands for Increased Sustainability Reporting

Never miss a thing.

Sign up to receive our insights newsletter.

As companies gather financial performance data to report on the prior year, more and more of them must also collect sustainability data. New reporting requirements continue to proliferate, which poses challenges to most companies. Even companies with mature ESG (environmental, social and governance) programs have to closely monitor changes. Better alignment and compatibility among ESG reporting frameworks have provided a smoother path for reporting. However, increasing reporting requirements outweigh the efficiencies gained.

Although managing multiple frameworks and aggregating data scattered across departments may initially seem daunting, you can organize your company’s processes to effectively and efficiently meet these requirements.

Why Does It Seem Like Demands for Sustainability Reporting Are Coming from Everywhere?

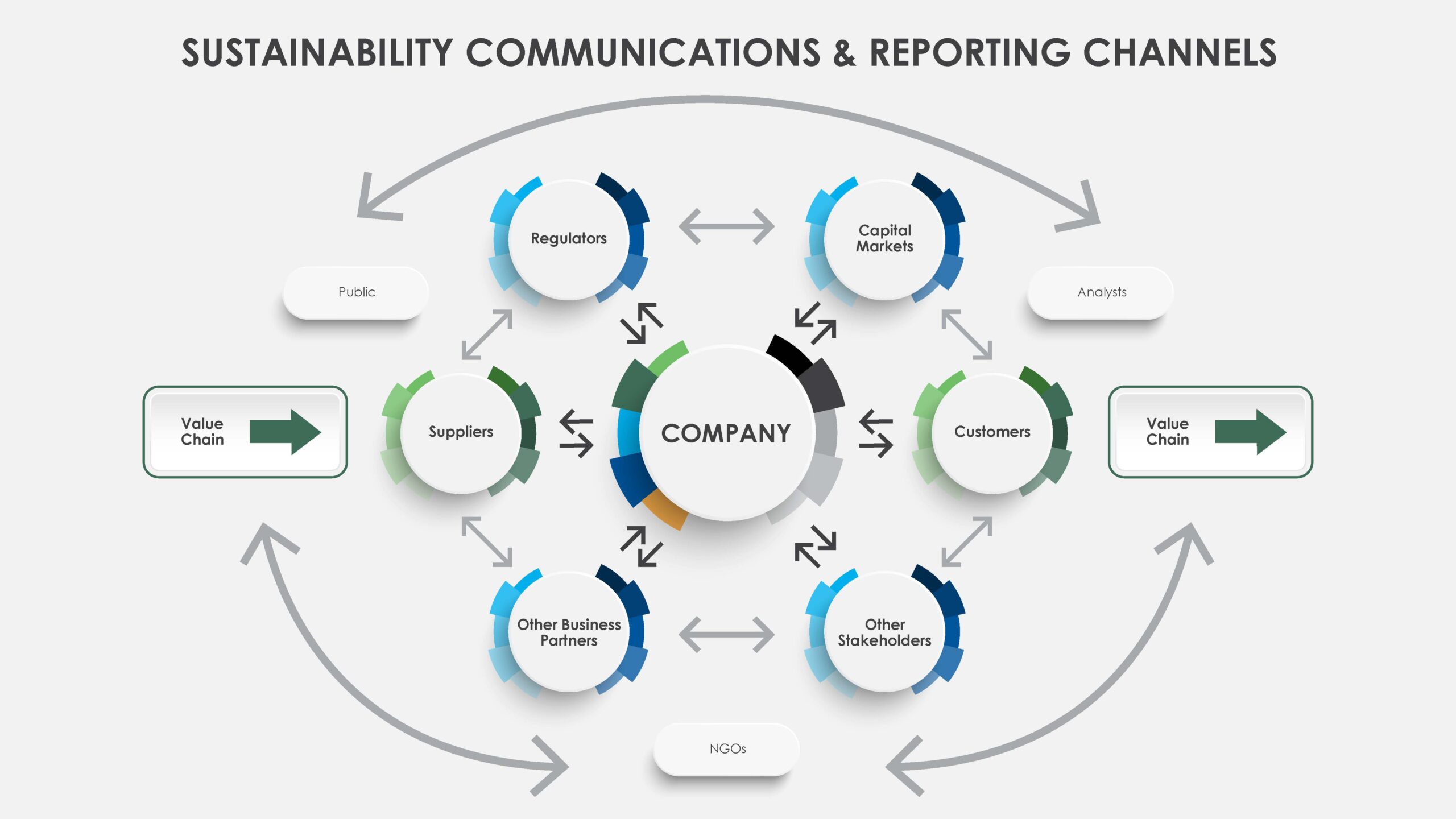

Because they are. Sustainability reporting started out as voluntary, designed to address the interests of disparate stakeholders: employees and prospective employees, customers and consumers, investors and local communities. Over time, some stakeholders became more interested in specific topics, including disclosure of climate risks to the organization, which resulted in reporting standards and frameworks for greenhouse gas (GHG) emissions; wage parity; product content and safety; and labor practices in the supply chain. Investors, in particular, recognized that sustainability strategy, risk management and performance — tailored to industry sectors — correlate to financial prospects. Furthermore, evaluating sustainability risk and performance requires participation from stakeholders up and down the value chain. As a result, companies are currently requesting sustainability data across their entire value chain using burdensome questionnaires, surveys and contractual obligations.

Is Sustainability Reporting Required?

In a word, yes, with more regulations on the way. This reporting began as voluntary efforts with standards set by non-governmental bodies, but over time more and more regulatory bodies have adopted requirements involving environmental and sustainability metrics.

Companies have long been familiar with compliance drivers for some sustainability reporting parameters, such as occupational safety statistics, workforce demographics and compliance with wastewater or other environmental permits. Now similar demands are being made for data involving GHG, corporate impacts on local communities, compliance with international labor standards and other more expansive information.

The Securities and Exchange Commission (SEC) has, for years, been discussing proposals for climate disclosures to be required of public companies, with a final rule adopted on March 6, 2024 (and immediately challenged in court). In preparation, the Sustainability Accounting Standards Board (SASB) developed standards that align with the common U.S. definition of financial “materiality.” Materiality is a concept that defines the significance of information to investors or other stakeholders. In the context of sustainability, significance is defined not only by impacts to the business, but to the environment and community as well.

While U.S. companies were waiting for the final SEC rule on climate-related disclosures, the International Sustainability Standards Board published global rules for reporting and disclosure on sustainability and climate. The EU’s Sustainability Reporting Standards will require mandatory reporting on a full range of environmental, social, and governance issues beginning the financial year 2025.

Although climate reporting demands are pervasive, requirements for transparency on social issues such as human rights are also on the rise. For example, companies doing business in the UK with annual turnover of approximately $50 million are subject to the UK Modern Slavery Act, which requires public disclosure of related risks in the supply chain.

Reducing GHG emissions continues to be a key global objective. As such, reporting of GHG emissions is required for some very large generators. Affecting the manufacturing sector, the Carbon Border Adjustment Mechanism requires importers of iron, steel, aluminum, cement, fertilizer, hydrogen and electricity in the European Union to report on the embedded emissions. In the U.S., California notably passed climate disclosure laws (Climate Corporate Data Accountability Act and GHG: Climate-Related Financial Risk) that will apply to many companies, both public and private, beginning in 2025. New York City narrowed its emissions reporting focus to owners of buildings larger than 25,000 square feet. If you are in the value chain of any company that sells into the EU or California, some requirements will ultimately find their way through the chain to you.

How Can Companies Know What Sustainability Reporting Is Required?

Companies should use well-defined processes to identify, evaluate, design, implement and monitor compliance programs for requirements that originate via law or regulation. These processes may include compliance registers, applicability analysis, scoping and both operational and documentation requirements. Expand the vision for these processes to accommodate the range of entities that require or expect sustainability reporting and disclosures. Consider including key voluntary sustainability reporting standards and frameworks, as well; historically, such “voluntary” standards have tended to become mandatory over time.

Developing a Reliable Approach to Sustainability Reporting

This could be a book, but here are a few tips to get you started:

- Learn about the reporting requirements, standards and frameworks that could affect your company. Understand how they apply to you directly (in your sector) and indirectly (via requirements originating from customers or business partners). Industry organizations and ESG reports from your peers are often good resources for this information, at least as a starting point.

- Formalize your processes and controls. Design, implement, test and improve processes and internal controls that involve ESG issues or data. COSO published a guide called “Achieving Effective Internal Controls over Sustainability Reporting (ICSR)” in March 2023. This supplemental guidance is designed to build a bridge between those who are familiar with “internal controls” (professionals in accounting, finance or internal audit) and those who are not (for example, people with environmental, human resources, procurement or real estate backgrounds). Departments less accustomed to internal controls are where much of the required sustainability data originates.

- Leverage technology. Sustainability reporting often begins with text documents, spreadsheets, chains of emails – or even sticky notes. Look for technology solutions that could help improve the reliability and timeliness of your sustainability reporting.

- Establish robust governance practices. Really, it all begins with good governance. Despite leaders’ best intentions, all these efforts can descend into chaos unless you have established clear responsibilities, accountabilities, communication and information flows. Build cross-functional teams with mandates and composition appropriate to the sector, business objectives and reporting requirements. Leverage specialists to improve the design and effectiveness of governance practices and the programs they touch.

- Align reporting practices with your business strategy and objectives. The demand for sustainability reporting has grown because stakeholders are asking for it. Companies that regard sustainability reporting only as a cost and a burden will prove themselves correct. On the other hand, organizations that align their strategies for sustainability programs with their larger mission and objectives will often find opportunities for financial or competitive advantage.

The proliferation of ESG reporting results from a heightened focus on sustainability in the business environment. As you chart a path to comply with mandates and satisfy expectations, strive to embed the solution into organizational goals to maximize value creation. Companies that build well-designed sustainability programs for responsible corporate citizenship, profitability and transparent reporting are positioning themselves for long term success.

Why Weaver?

Our experienced professionals understand sustainability reporting and can assist at every stage of the ESG journey. With services tailored to the industry and organization; Weaver can drive processes and strategies that maximize impact. Rely on our professionals to assess the latest sustainability regulations and trends for matters that are most relevant to your business. We offer a comprehensive suite of services aimed to simplify complex disclosure requirements like GHG Emissions and provide confidence in the delivery of investor-grade data. Contact us to discover how we can craft solutions, helping you innovate today for tomorrow’s success.

© 2024

Weaver is pleased to have Douglas Hileman as a guest contributor in collaboration with Ashly Pleasant, Director of Sustainability Services & ESG. Doug is an author of COSO’s supplemental guidance on sustainability reporting; he has decades of experience in sustainability, compliance, risk and auditing.