Economic Nexus Since the Wayfair Decision: Frequently Asked Questions About Sales and Use Taxes (Part 1)

The South Dakota v. Wayfair, Inc., decision and economic nexus laws have changed the landscape for taxpayers who sell tangible personal property or provide services that are subject to sales and use taxes. This new landscape has increased the administrative burden on taxpayers and their filing and reporting requirements.

Weaver’s four-part series of frequently asked questions will help you understand this new sales tax landscape and how it may impact your company.

Part 1: Is My Company Affected by New Economic Nexus Laws?

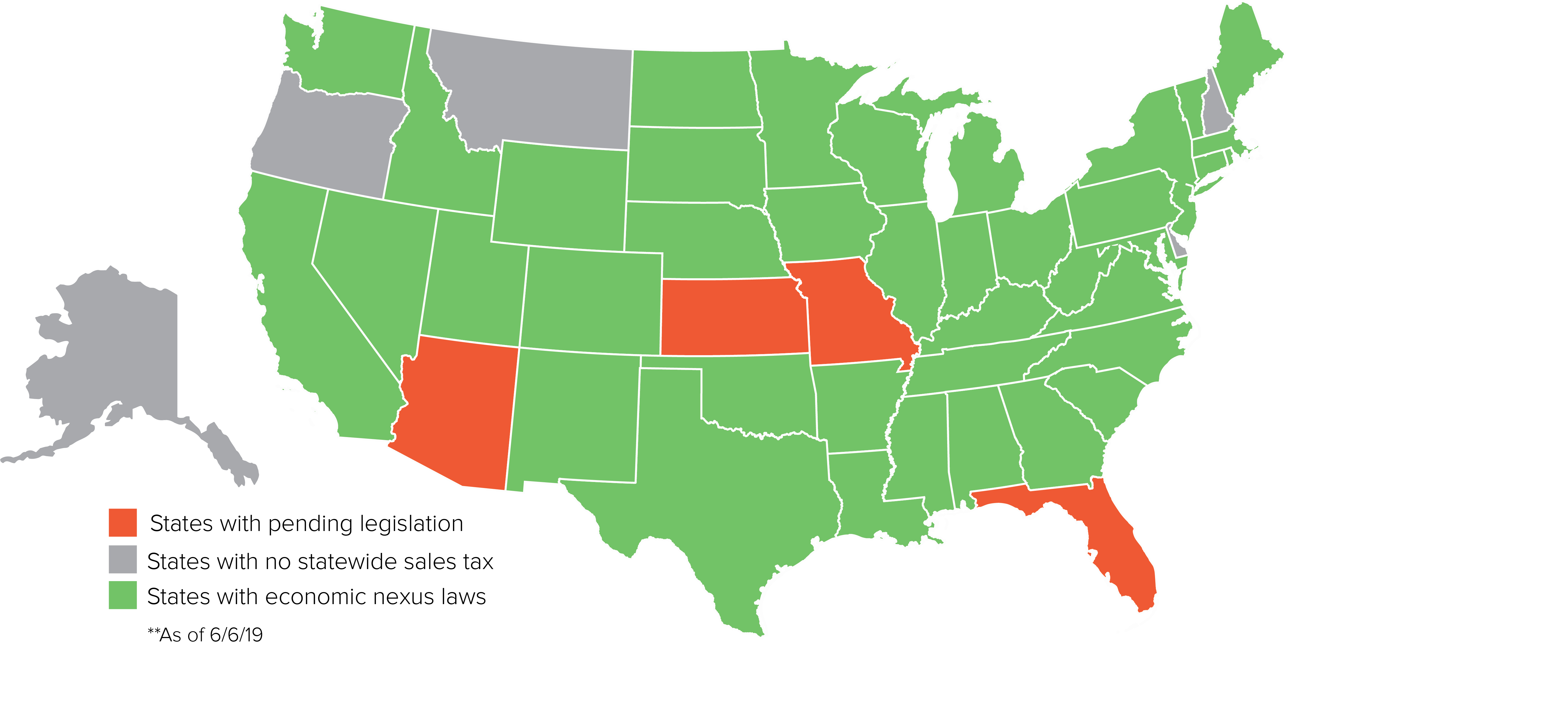

How many states have passed economic nexus sales and use tax laws like South Dakota?

In the United States 42 jurisdictions (41 states + Washington D.C.) have passed economic nexus laws for sales and use tax. Five states do not have a statewide sales tax: Alaska, Delaware, Montana, New Hampshire and Oregon. Four states with statewide sales tax — Arizona, Florida, Kansas, and Missouri — have pending or proposed legislation to implement economic nexus.

Which sales are used to determine economic nexus thresholds?

It will depend on the state. Some states use gross sales (retail and wholesale) to determine nexus thresholds and other states use retail sales only. Furthermore, some states only subject those who sell tangible personal property to the thresholds; service companies, such as cloud-based software providers, are exempt.

What time frame do I use to calculate thresholds?

Most states have specified calendar year 2017 as the first period, or January 1, 2018, to the present as the second period. If you met the threshold in 2017, you are expected to begin filing by the effective date. If you did not meet the thresholds in 2017, but meet the thresholds during 2018 or 2019, most states require you to begin reporting within a specified number of days after reaching the threshold.

When evaluating the economic nexus threshold, do I review “Customer Bill to Location” or “Customer Ship to Location”?

Easy answer — the “ship to” location.

Are the thresholds for economic nexus based on the total value of sales in dollars, or on the number of transactions?

It depends on the state. Some states only have a dollar-amount threshold. Other states have a threshold for either transaction count or dollar amount.

These regulations change often, so in addition to monitoring changes in which states have economic nexus laws, companies need to monitor the thresholds in states where they have sales. The Sales Tax Institute maintains a useful online reference.

What is a “transaction”?

Most states have not defined the term “transaction.” Until further guidance is released, it is recommended you assume a transaction is an invoice or billing, rather than individual items listed on the invoice.

Does the Wayfair ruling affect traditional “physical presence” nexus?

Traditional nexus can still be established through sufficient physical presence in a jurisdiction, such as a warehouse, retail outlet or office.

We do not have the people, time or expertise to keep up with these rules and make sure we are complying in every state. What should we do?

Weaver can help. Our clients lean on our experience to guide them through the numerous new state laws, so they can stay on top of requirements that affect them. Weaver’s state and local tax team has been busy performing economic nexus studies to give our clients a clear picture of their new filing obligations in this new, post-Wayfair environment. If you would like to discuss your situation and learn how Weaver can help you, please schedule a complimentary consultation with our team.

Read more from our “Frequently Asked Questions” series: