PPP Loan Forgiveness: What Banks Should Consider in Their Controls

The Paycheck Protection Program (PPP) has proven to be both a significant challenge and monumental opportunity for community banks. Banks have successfully navigated the uncertainty stemming from a lack of clear guidance and the demands of extremely high volume. As the initial rounds of PPP funding are now largely completed, banks are turning their focus to forgiveness.

On May 15, 2020, the Small Business Administration (SBA) released loan forgiveness forms and instructions, which provide some clarity for borrowers and lenders. Banks can now think more specifically about the forgiveness phase.

In establishing a framework for processing loan forgiveness calculations, it is important for banks to remember who has ultimate responsibility for accuracy of loan forgiveness: the borrower. The SBA Interim Final Rule states, “The lender does not need to conduct any verification if the borrower submits documentation supporting its request for loan forgiveness and attests that it has accurately verified the payments for eligible costs. The Administrator will hold harmless any lender that relies on such borrower documents and attestation from a borrower.”

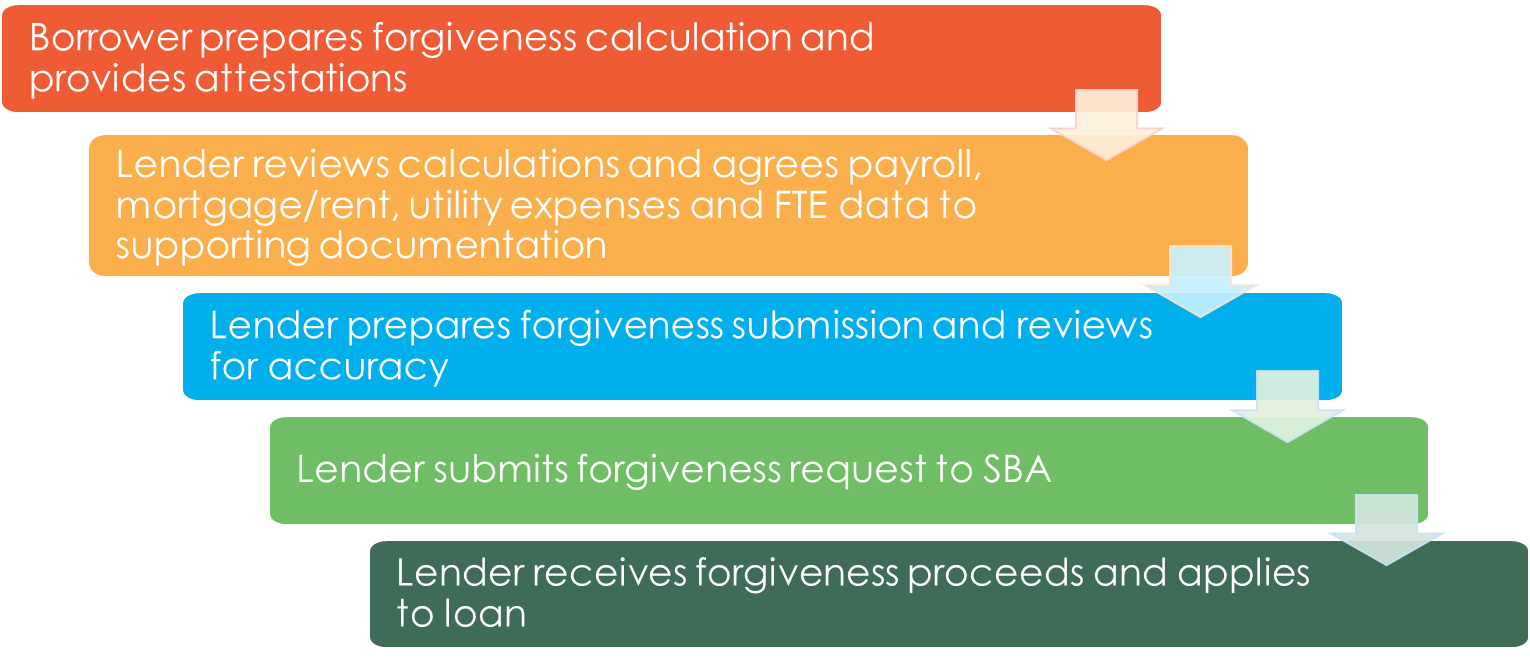

Accordingly, loan forgiveness processes and controls should primarily focus on completeness of documentation and performance of necessary reviews and monitoring. For most lenders, the loan forgiveness process will include the following steps:

To support forgiveness calculations, banks should require the following documentation (at a minimum):

- Forgiveness application

- PPP Loan Forgiveness Calculation Form

- PPP Schedule A

- Payroll documentation

- Form 941

- Payroll register

- Rent/mortgage documentation

- Mortgage amortization schedules

- Rent agreements

- Statements

- Evidence of payments

- Utility expense documentation

- Invoices

- Evidence of payments

Specific instructions regarding required documentation are included with the SBA Loan Forgiveness Application Instructions for Borrowers.

To minimize bank risks in the forgiveness process and put customers in the best position should their loan be selected for audit, banks should consider the following controls:

- Regular review of exception reports to ensure ticklers for receipt of eight-week documents and forgiveness calculations are timely addressed. Educate your borrowers on what documentation will be required of them and when documentation is expected, and perform a frequent review of exception reports to ensure borrowers provide timely documentation. Contact borrowers immediately if they fail to submit applications and supporting documentation timely or if documentation is incorrect or incomplete.

- Secondary review of borrower loan forgiveness calculations for agreement to source documentation and accuracy of SBA system input. Banks are responsible for reviewing the PPP Loan Forgiveness Calculation Form and PPP Schedule A for completeness, agreeing amounts to supporting documentation, and verifying the mathematical accuracy of documented calculations. Additionally, banks should perform a secondary review of E-Tran input for accuracy and agreement to the Loan Forgiveness Calculation Form.

- Use of a forgiveness checklist to ensure completeness of documentation and reviews. Use a checklist or workflow to ensure required documentation is received from borrowers. Bank personnel can also use it to ensure the application, calculation, and SBA submission are performed and formally documented.

- Review of forgiveness pipeline to ensure forgiveness submissions are made timely. Banks have 60 days to review borrower forgiveness requests and submit to the SBA. To ensure completeness and timeliness of forgiveness submissions, banks should establish pipeline reports documenting date requests were received with dates due to the SBA. These reports should be reviewed daily to ensure no submissions are missed.

- Performance of reviews to ensure forgiveness proceeds are properly received and applied to loan balances. The SBA has 90 days to review forgiveness submissions and remit forgiveness proceeds. Banks should regularly review and reconcile the account used for SBA proceeds as well as the PPP loan trial balance to ensure proceeds are received timely and are properly applied to loan accounts. Because of the volume of proceeds that may occur, banks may also consider establishing a secondary review of payment posting entries to ensure the accuracy of payment applications.

If you would like to talk through your processes, assess your controls, or ask questions about your loan forgiveness processes, contact us.

© 2020