For-Profit Freestanding IRF Joint Venture Growth: Assessing Opportunities, Risks and Valuation Perspectives

Health Care Valuation Services

Health Care Valuation Services

Never miss a thing.

Sign up to receive our insights newsletter.

Inpatient rehabilitation facilities (“IRFs”) provide intensive rehabilitation services to patients after illness, injury, or surgery. Rehabilitation programs include services such as physical therapy, occupational therapy, rehabilitation nursing, speech-language pathology, and orthotic services.

During the pandemic, IRFs illustrated their crucial benefit to the healthcare system by caring for COVID patients as well as other patients with complex, high-acuity care needs. IRFs have educated referral sources about their proven clinical value (i.e. lower hospital readmission rates and better clinical outcomes).

IRFs can be freestanding (typically larger footprints) or hospital-based. Hospital-based IRFs are often smaller and occupy one or two floors within the acute care hospital. Joint ventures between health systems and specialized freestanding IRF operators continue to proliferate. Encompass Health, the largest freestanding operator of IRFs, has health system joint venture partners for 38% of its 159 rehabilitation hospitals.

As health systems strategically move their hospital-based IRFs to a separate freestanding facility, additional space for acute care patients becomes available while the system is able to maintain or expand the profits and benefits from integrated IRF capabilities. In turn, freestanding operators are able to align with their primary patient referral base.

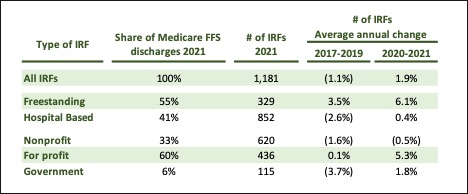

By the Numbers

According to data from MedPac released in March 2023, recent growth of new for-profit freestanding IRFs was particularly robust.

Based on the MedPac data:

- A low discharge rate of presumptively eligible patients from an acute care hospital to an IRF indicates that there is a large addressable market. In addition, favorable demographics are driving increased demand for rehabilitation services.

- Annual growth in the number of IRFs during 2021 is concentrated in freestanding structures (+6.1%) and for-profit ownership (+5.3%).

- Freestanding IRFs have higher total discharges even though there are significantly fewer freestanding facilities than hospital-based. Freestanding IRFs processed 55% of all discharges in 2021 while accounting for only 28% of all facilities.

- For-profit IRFs make up 34% of all facilities but account for 60% of the total discharges.

- Note: Encompass Health is the largest owner-operator of for-profit IRFs and have ~160 facilities, representing ~36% of total for-profit IRFs.

Yes, But…

- Some inpatient rehabilitation services can be performed in less expensive settings. According to MedPac, the absence of IRFs in some areas of the country suggests that Medicare beneficiaries that do have access to IRFs could receive similar services in other, and perhaps less expensive, settings.

- Historically, Medicare has not scrutinized IRF reimbursement because the industry represents a small percentage of the overall spend. However, from a reimbursement perspective, IRFs are the most expensive post-acute care setting. The industry’s growth creates a risk that Medicare (representing the majority total discharges) will lower reimbursement or further restrict patient eligibility. For example, due to the industry’s success, MedPac’s 2023 report recommended a 3% decrease in the base IRF payment rate.

- Joint ventures between hospital systems can be very effective in aligning hospital system interests while allowing specialized experts to focus on patient care. However, these businesses must be properly “wired” prior to formation, ensuring financial and clinical objectives are aligned and commensurate to each partner’s ongoing risks and contributions. A misalignment may result in an unbalanced and unsustainable joint venture.

Health Care Valuation Takeaways

- Valuations are often needed to establish JV ownership percentages based on what each party initially contributes. When the book-of-business from hospital-based IRFs is contributed, the valuator should take special cautions. Hospital-based IRF departmental financials often require adjustments to reflect their true performance as a stand-alone entity. Valuators should:

- Validate qualifying patient volume and revenue-per-patient-day by payor to ensure continuity and accuracy,

- Understand the potential restrictive effects of Medicare Advantage current penetration and growth in the local market. Medicare Advantage plans may be more or less aggressive in steering members to lower-cost settings for post-acute care (i.e. SNFs, outpatient rehab, etc.), which makes patient admissions to IRFs more challenging.

- Ensure the hospital-based IRF departmental income statements are fully burdened with expenses by confirming adequacy of staff, facility, supply and overhead costs.

- Assess the sustainability of IRF referral sources and, depending on the local market, understand the potential impact of new entrants and competitors to this highly attractive space.

- Understand how the pandemic affected the clinical and financial performance of IRFs, and how to adjust financial performance as clinical patient flows normalize.

- Joint ventures can be very effective in accomplishing the goals set forth by the parties; however, the transaction must be carefully planned to ensure the long-term alignment of incentives. Any upfront valuation of relative (or absolute) contributions is key to the equation and must be carefully planned and executed.

For more information about these observations and the effect on health care valuations, contact us or visit our health care valuation and transaction advisory services page.

©2023

This is one in a series of related health care valuation posts: