2024 Q2 Accounting and SEC Update

Never miss a thing.

Sign up to receive our insights newsletter.

Weaver’s second quarterly Accounting and SEC Update of 2024 covered stock compensation and other standards updates, filer status assessments, and recent SEC and PCAOB enforcement actions.

Accounting Standards Updates

In March 2024, the Financial Accounting Standards Board (FASB) issued ASU 2024-01 Stock Compensation as an update to existing ASC 718 requirements. The ASU improves existing guidance in this area by adding illustrative examples to demonstrate how an entity should apply the scope guidance in paragraph 718-10-15-3. Amendments in this paragraph improve its overall clarity and operability without changing the guidance.

ASU 2024-01 is effective for public companies for annual periods beginning after December 15, 2024, and interim periods within those annual periods. For all other entities, it is effective for annual periods beginning after December 15, 2025, and interim periods within those annual periods. Early adoption is permitted.

ASU 2024-02: Codification Improvements, which the FASB also issued in March 2024, removes references to various FASB Concepts Statements, as, among other reasons, they are extraneous and not required to understand or apply codification guidance. By removing all references to Concept Statements in the guidance, the FASB simplified the codification and distinguished authoritative and nonauthoritative literature.

ASU 2024-02 is effective for public companies for fiscal years beginning after December 15, 2024. For all other entities, it is effective for fiscal years beginning after December 15, 2025. Early adoption is permitted. If an entity adopts the amendments in an interim period, it must adopt them as of the beginning of the fiscal year that includes that interim period.

PCAOB Standards Update

PCAOB Update: QC 1000 replaces a set of quality control (QC) standards that the accounting profession issued before the PCAOB was created. It requires all registered firms to establish quality objectives, identify and assess quality risks, and design responses. Firms that perform engagements under PCAOB standards will be required to implement and operate QC systems and report their results annually to the PCAOB via a new, non-public reporting form called “Form QC.”

The new standard will take effect on December 15, 2025, following SEC approval.

Reporting Reminders

Executives should ensure that they are familiar with new SEC rules that may affect their organization. We discussed recently issued rules including share repurchase disclosure modernization and changes to Regulation S-P, which expands the requirements for policies and communications regarding protection of consumer financial information. We also discussed the following topics:

Cybersecurity

Smaller reporting companies (SRC) must now file a Form 8-K to comply with the SEC’s cybersecurity rules regarding disclosure of material incidents. The additional 180 days for SRCs to comply with Form 8-K Item 1.05, Material Cybersecurity Incidents, after the initial effective date of December 18, 2023 has passed.

Companies must file the Form 8-K within four days of determining that an incident was material. Firms must disclose the nature, scope and timing of an incident as well as the impacts, or reasonably likely impacts, of the incident.

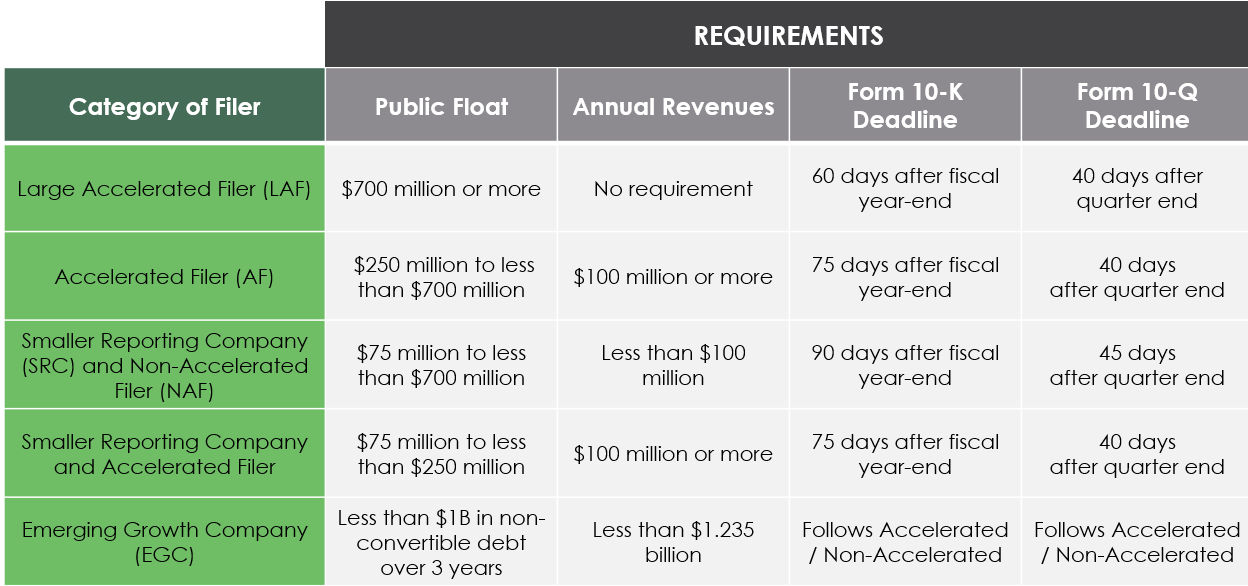

Filer Status

A public company’s filer status drives its filing timelines, financial statement requirements, effective dates for the adoption of certain SEC regulations, and Sarbanes-Oxley requirements. Non-accelerated filers are not subject to Section 404(b) requirement to obtain an audit report on ICFR.

Filing Status Overview (Initial Measurement)

For subsequent remeasurements, a company’s revenues and/or public float metrics would have to decrease below 80% of the initial measurement thresholds to change its filer status.

Measurement: When to Measure?

The determination of filer status occurs at the end of the issuer’s fiscal year. Changes impact annual filings and subsequent quarterly and annual filings. Annual revenue measurements are based on the most recently completed fiscal year for which audited financial statements are available.

Public float is measured on the last business day of the second fiscal quarter (i.e., June 30 for calendar year-end companies). Remember, public float is the aggregate market value of an issuer’s outstanding voting and nonvoting common stock held by non-affiliates.

Potential Consequences

While certain automatic extensions exist for filers with the filing of appropriate forms, failure to comply with filing deadlines could have severe potential consequences, including:

- Monetary fines

- Regulatory investigation

- Shareholder lawsuits

- Delisting from stock exchanges

- Rendering existing registrations ineffective

Emerging Growth Companies

Companies may qualify as an emerging growth company (EGC) upon becoming a public company, and may retain that status for up to 5 years if they continue to meet the following qualifications:

- Total annual gross revenues of less than $1.235 billion during the most recently completed fiscal year

- Not issued more than $1 billion of non-convertible debt in the past three years (ongoing assessment)

- Not qualify as a large accelerated filer

Pro Forma Financial Information

Companies must present pro forma financial statements under Regulation S-X, Article 11 under the following conditions:

- A significant acquisition of a business has occurred

- Consummation of a significant business acquisition has occurred, or is probable, subsequent to the most recent period end

- Disposition of a significant portion of a business (sale, spin-off, split-up or split-off) has occurred or is probable

- Roll-up transactions have occurred

- Other transaction has occurred, or is probable, for which disclosure of pro forma financial information would be material to investors

Companies report the pro forma information in Item 2.01 of Form 8-K, along with the audited financial statements of an acquired business as required (with an automatic 71-day extension for acquisitions in most instances), as well as in registration statements and certain proxy statements. The financial information required under Article 11 includes:

- Balance sheet (most recent balance sheet date reported)

- Statements of comprehensive income (most recent annual period, and subsequent year-to-date interim period)

- Accompanying explanatory notes describing adjustments

This includes the effects of purchase accounting; debtor equity financing to complete the acquisition; amortization/depreciation adjustments; transaction costs and certain compensation arrangements; and management’s adjustments.

What is considered “Significant” for Pro Forma Requirements?

An acquisition or disposal of more than 20% is significant to a registrant based on an asset, investment or income test, and triggers pro forma financial statements. Pro formas are also required if an acquired business of the registrant consummated a significant acquisition of its own during the year (if material to registrant).

A company must also consider the aggregate of transactions that are not individually significant. If the aggregate significance is more than 50% for any test, then the transactions are included in the pro formas as the aggregate effect of all individually insignificant transactions.

ASC Topic 805- Business Combination Pro Forma Requirements

While Article 11 provides requirements for certain filings, companies also must remain aware of the disclosure requirements in their periodic filings under ASC 805. Requirements under ASC 805 are substantially less detailed than those in Article 11, with ASC 805 generally requiring only revenue and earnings information. It does not provide explicit guidance on pro forma adjustments, resulting in companies typically using the guidance in Article 11.

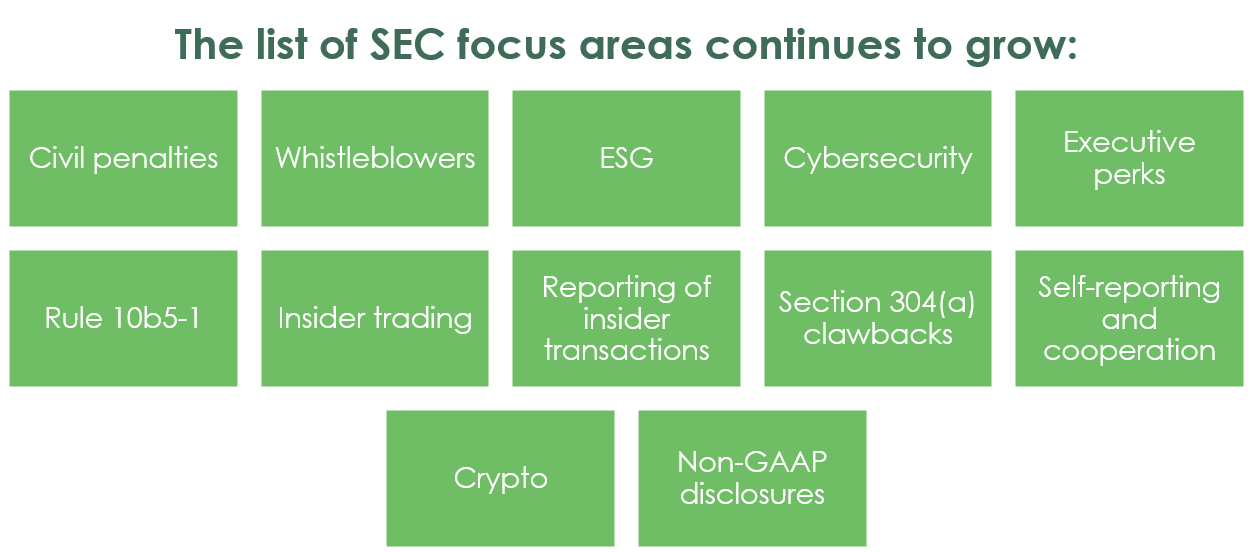

Regulatory Environment Update

SEC Enforcement

The SEC is focusing its enforcement efforts on misleading information, internal controls and accountability.

The SEC was aggressive in enforcement in 2023. There were 784 enforcement actions (+3% YoY) and the $4.95 billion in financial remedies was the second highest ever. The commission barred 133 individuals from serving as officers/directors and awarded $600 million in its whistleblower program.

The SEC is on a similar pace in 2024 with new resources and capabilities. Companies, however, are increasingly willing to challenge the SEC in response to its aggressive approach.

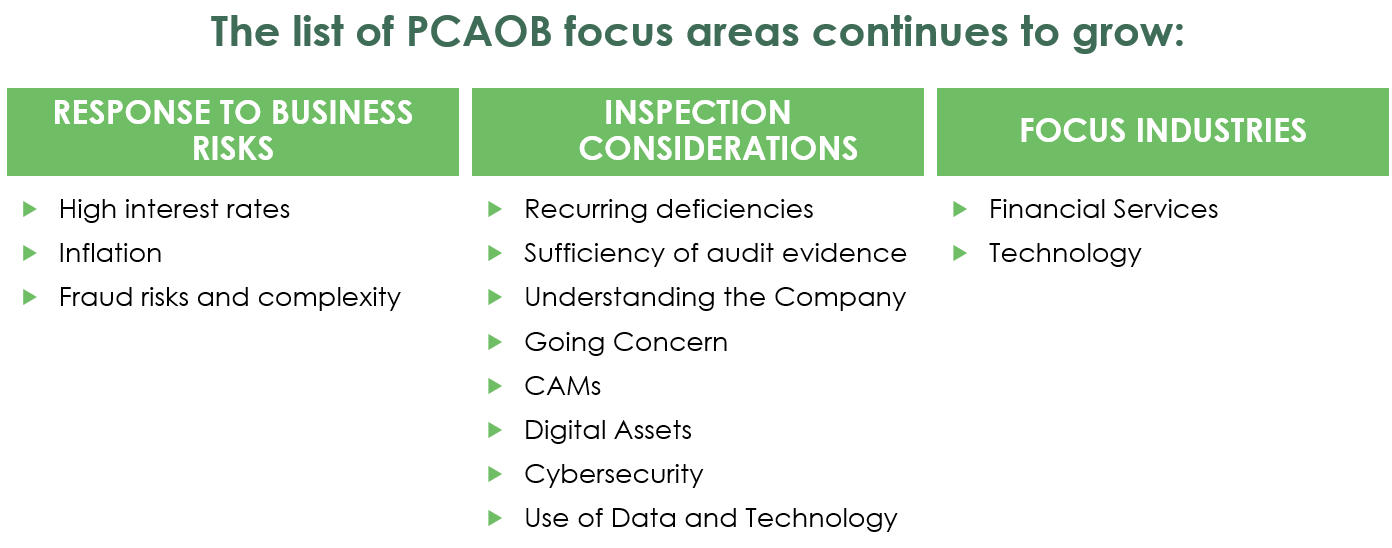

PCAOB Enforcement

In the News – AI Washing

The SEC is looking at companies engaged in “AI washing” in which they exaggerate or misrepresent their use of artificial intelligence (AI) to attract investors. Companies must ensure that their messaging is accurate and be aware of false or misleading statements. In March 2024, there were two enforcement actions due to false and misleading statements on the use of AI.

In the News – Crypto

ASU 2023-08 Intangibles – Goodwill and Other – Crypto Assets (Subtopic 350-60)

Companies will measure cryptocurrency at fair value with changes through earnings. Fair value determination is challenging, as there are variable inter-day price swings. Nonetheless, this is an improvement over the previous treatment, which recognized impairment loss without recognizing gains. The ability to recognize gains is expected to increase investment from institutional investors and public companies.

The standard is narrow in scope and challenging for out-of-scope assets. To be in scope, the asset must meet the following criteria:

- Intangible asset

- Secured through cryptography

- Created or resides on a distributed ledger

- No rights to other assets

- Not created by the entity or a related party

- Fungible

The SEC stance has taken the position that regulation for stocks and bonds should apply to crypto, while other regulators want crypto assets to be distinct from stocks and bonds. The SEC, however, has had several legal victories against challenges that it has over-regulated and violated investor-protection rules.

Next Steps

Weaver’s accounting and technology advisors offer companies several ways to learn more about building their paths forward during Weaver’s Quarterly Accounting and SEC Update webinars, within their podcast series, and in their Executive Resource Center. To discuss your unique circumstances, we encourage you to contact us directly to schedule a consultation.

©2024