Accounting & SEC Update: 2023 Fourth Quarter

Never miss a thing.

Sign up to receive our insights newsletter.

Weaver’s fourth quarter Accounting and SEC Update closed out 2023 by highlighting several key changes during 2023 that deserved special attention. Fewer regulatory updates in Q4 allowed us to provide a deeper dive into ESG Climate and Emissions regulations before we delved into providing guidance for 2023’s year-end.

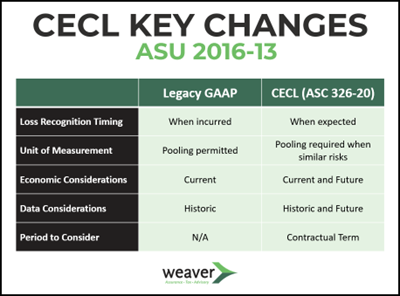

Current Expected Credit Losses (CECL) – (ASC 326)

Smaller Reporting Companies (SRCs) were required to begin following CECL on January 1, 2023, after earlier implementation by larger entities. CECL significantly impacts the methods and current practices used to recognize impairment of financial assets, based on the premise that impairment should be evaluated on expected credit losses, rather than incurred losses.This standard also simplifies some elements of previous U.S. GAAP with its shift to a principles-based approach, and by decreasing the number of potential models for certain instruments.

For year-end, companies should evaluate whether their previous analyses and interim disclosures will be sufficient to meet the requirements for their 10K, and be prepared for potential increased scrutiny as they navigate their year-end audits.

While CECL provides flexibility on the nature and extent of the disclosures you provide, ensure that lengthy forecast periods and macroeconomic factors that contribute to your decisions are included within your analysis, allowances, and disclosures.

ASUs Effective in 2023

Many of the ASUs that became effective in 2023 are industry-specific. They’re still important to be aware of since many affect your business partners and contracts.

- ASU 2017-04 – Intangibles – Goodwill and Other (Topic 350)

- ASU 2018-12 – Financial Services – Insurance (Topic 944)

- ASU 2021-01 – Reference Rate Reform (Topic 848)

- ASU 2021-08 – Business Combinations (Topic 805)

- ASU 2022-04 – Liabilities – Supplier Finance Programs (Subtopic 405-50)

Enhancing transparency through more detailed disclosures is certainly a theme we’re seeing that won’t end anytime soon.

Two additional ASUs issued in 2023 provide interpretive guidance on SAB 120 and SAB 121.

- ASU 2023-03 – “Spring loaded” Share Base Payment Awards

- ASU 2023-04 – Liabilities – Crypto assets

Several ASU bulletins became effective for those with fiscal years ending December 15, 2023, and onward which should be reviewed to ensure compliance for 2024 transactions, measurements, and disclosures. ASU 2023-07 on Segment Reporting (Topic 280) is particularly applicable for many businesses, with its requirements to enhance incremental segment information to provide greater alignment of interim reporting with 10K details.

Final SEC Cybersecurity Rule

Incident Disclosures

With the exception of SRCs, SEC registrants must now comply with the new incident disclosure requirements as of December 18, 2023. SRCs were given a little more time and must fully comply by June 15, 2024. Material Cybersecurity incidents must be disclosed via Form 8-K within four days of being deemed as such.

Existing frameworks can aid companies in evaluating materiality from both quantitative and qualitative perspectives. Be sure that your processes, controls, and protocols are in place for identifying them, evaluating them for materiality, and getting any disclosures out to the public that are necessary.

Note: Weaver did a deep dive into Cybersecurity regulations during our third quarter Accounting and SEC Update. Review our summary and watch the webinar for greater detail and discussion on the topic.

Annual Disclosures

The SEC’s Cybersecurity regulations added Item 106 to Regulation S-K describing the extensive annual disclosures that are now needed for all annual reports for fiscal years ending on or after December 15, 2023. These disclosures involve significant coordination and review outside of the finance teams, so the wheels should already be in motion for upcoming 10-Ks.

Clawbacks of Executive Compensation

Incentive compensation that was based on financial reports that have since been restated are covered in the SECs final rule of Item 402. The regulation includes both the reissue of previously filed 10Ks or 10Qs as well as corrections of prior periods. While this ruling isn’t new, it is coming into play more as we move further from its 2022 effective date and major exchanges have implemented their policies.

Any performance or financial-based metrics that were used to determine the amount of executive compensation—share-based awards, retirement plan contributions, etc.—are within scope of this clawback rule. Security exchanges were required to adopt listing standards to hold issuers accountable for developing and implementing policies that provide for the recovery of erroneously awarded compensation.

Share Repurchase Disclosure

Those within—or preparing for—a share repurchase cycle should keep in touch with counsel regarding preparing for the disclosure requirements. The SEC amendments for disclosing share repurchases in its current state was overruled in the U.S. Court of Appeals but will certainly be appealed or modified to address the identified defects.

SEC Comment Letter Trends

The volume of comment letters on Company’s periodic filings (Form 10-Ks and 10-Qs) has sharply increased in 2023. Many topics are consistent with the historic focus areas—revenue recognition, MD&As, business combinations, etc.—with newer regulations on climate change and ESG regulations becoming more prominent.

- Non-GAAP measures should not be given emphasis over GAAP—such as EBIDTA metrics over net income. Include reconciliations to explain the variances and the importance to the company of disclosing non-GAAP measures.

- Management Discussion and Analysis is an opportunity for business leaders to share their perspective on recent activity as well as industry-affecting trends that they see as relevant and significant.

- Providing clarity with robust disclosures around obligations, patterns, and recognition can help you maintain compliance despite the subjectivity involved in many of today’s principles-based regulations.

ESG – Climate & Emissions Update

Corporate responsibility is the foundational bedrock of ESG (environmental, social and governance principles; leveraging frameworks to guide the disclosure of the impacts of corporate activity in relation to society and the environment in which it operates. Talent retention, access to capital, and regulatory compliance are just some of the positive outcomes and opportunities resulting from implementing meaningful ESG programs.

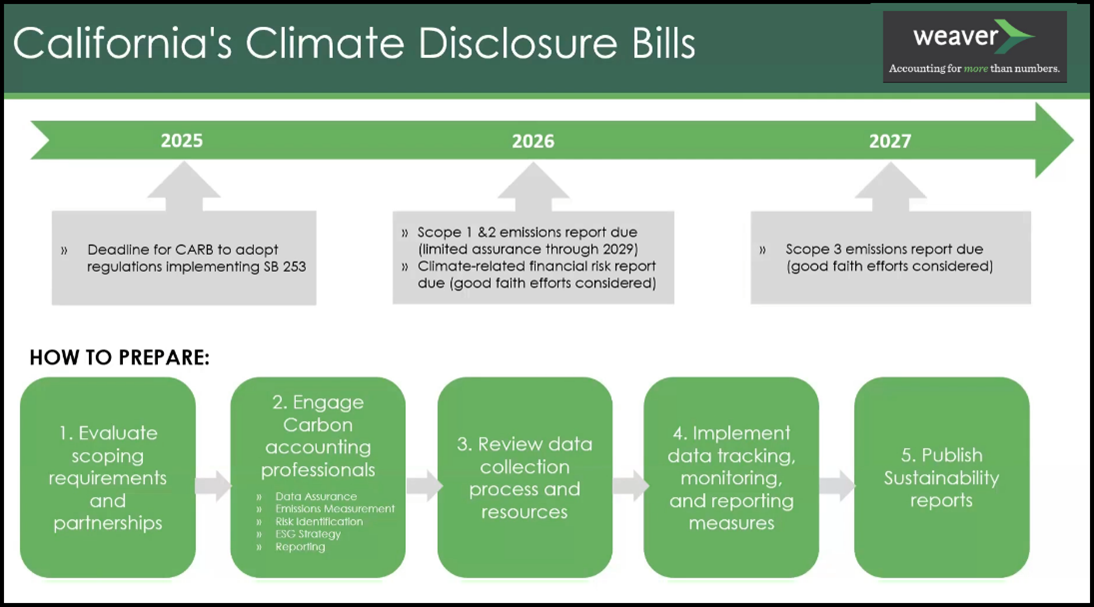

California – the fifth largest economy in the world— has positioned itself as a trailblazer by passing the first of its kind legislation in the U.S.; requiring business to report their GHG emissions and climate related risks It is more pervasive than the proposed SEC regulations as the scoping criteria encompasses both public and private companies.

- California’s Senate Bill 253 – the Climate Corporate Data Accountability Act, requires the disclosure of Scope 1 & 2 greenhouse gas emissions (GHG) by January 2026 and Scope 3 by January 2027 from entities that do business in California and have over $1 billion in total annual revenue. Penalties for noncompliance can be assessed up to $500k per reporting year.

- Third-party assurance partners are required in order to ensure that accurate and complete data is being submitted. The bill details various qualifiers for third-party firms, so it is important to verify they are reputable and align with the specified standards.

- Senate Bill 261, The Climate-Related Financial Risk Act, applies to entities doing business in California with over $500 million in annual revenue to bi-annually disclose climate related financial risks, measures, and reporting gaps to the California Air Resources Board (CARB) beginning in January 2026. As with SB 253, those found in violation of SB 261 may be penalized up to $500k per reporting year.

- Assembly Bill 1305, the Voluntary Carbon Market Disclosure Act, requires those that make carbon offset claims to disclose detailed information supporting their claims on the entity’s website. There is no revenue threshold, and the Act has an effective date of January 1, 2024. As a result, all entities doing business in California that make any carbon offset, zero-emissions, or GHG reduction claims may be subject to $2,500 per day in fines if they are not compliant.

Year-End Tax Essentials

Estimates and disclosures continue to be the theme to focus on.

- Provisions for Return Adjustment – Now is the time to have discussions with auditors about variances between the prior year income tax provision and the as-filed federal and state income tax returns. It is important to determine whether the variances are merely a change in estimate or an error. Documentation around these determinations is critical to the audit of the income tax provision.

- Section 162(m) Compensation Deduction Limitation – Analyze equity compensation arrangements with covered employees to determine if Section 162(m) compensation deduction limitations may be triggered. Additionally, given the strong equity market in 2023, it is likely that there will be windfall tax benefits to be considered when calculating the effective tax rate.

- ASU 2023-ED100 – FASB approved this exposure draft to increase the granularity around ASC 740 tax reporting disclosures. It requires significant effort to achieve the granularity specified as well as qualitative disclosures to reconcile the statutory tax rate and effective tax rate. A number of organizations have petitioned FASB to reconsider this ASU due to the perceived cost of implementation and ongoing reporting efforts versus its potential benefits.

- State Tax Law Changes – It is important to consider state tax law changes that have taken effect during the reporting period to analyze any impact on the overall state tax rate. Many states are also adopting new tax regimes to address the growing use of pass-through entity tax filing elections.

Next Steps

Whether provisions mandate third-party assessments or reason dictates that it’s prudent to obtain guidance on new compliance standards, Weaver is here to help.

Our advisors monitor regulations to ensure compliance as we conduct comprehensive tax and financial planning. Our ESG team can work with you to develop your strategy, provide investing guidance, and deliver the knowledge necessary for third-party assurance. Contact us today to find a partner that cares about your most pressing needs.

©2024

Weaver’s Accounting and SEC Update

Sign up for our quarterly series to stay informed!