Powering AI Infrastructure: Energy Supply and Carbon Transparency Challenges

Never miss a thing.

Sign up to receive our insights newsletter.

The rapid growth of artificial intelligence is reshaping digital infrastructure and energy markets. As computing capacity demand accelerates, data center developers must balance speed-to-power with increasing expectations around reliability, carbon transparency and regulatory oversight.

In the near term, natural gas (NG) — particularly through behind-the-meter solutions — is emerging as a practical way to meet accelerating power demand while grid infrastructure and renewable capacity continue to expand. At the same time, advances in emissions monitoring, differentiated gas markets and carbon accounting frameworks are giving organizations new tools to manage both operational and environmental performance.

Developers that integrate energy strategy, carbon transparency and market risk management into their planning will be better positioned to scale AI infrastructure responsibly while meeting the expectations of investors, regulators and compute buyers.

The AI-Driven Energy Challenge

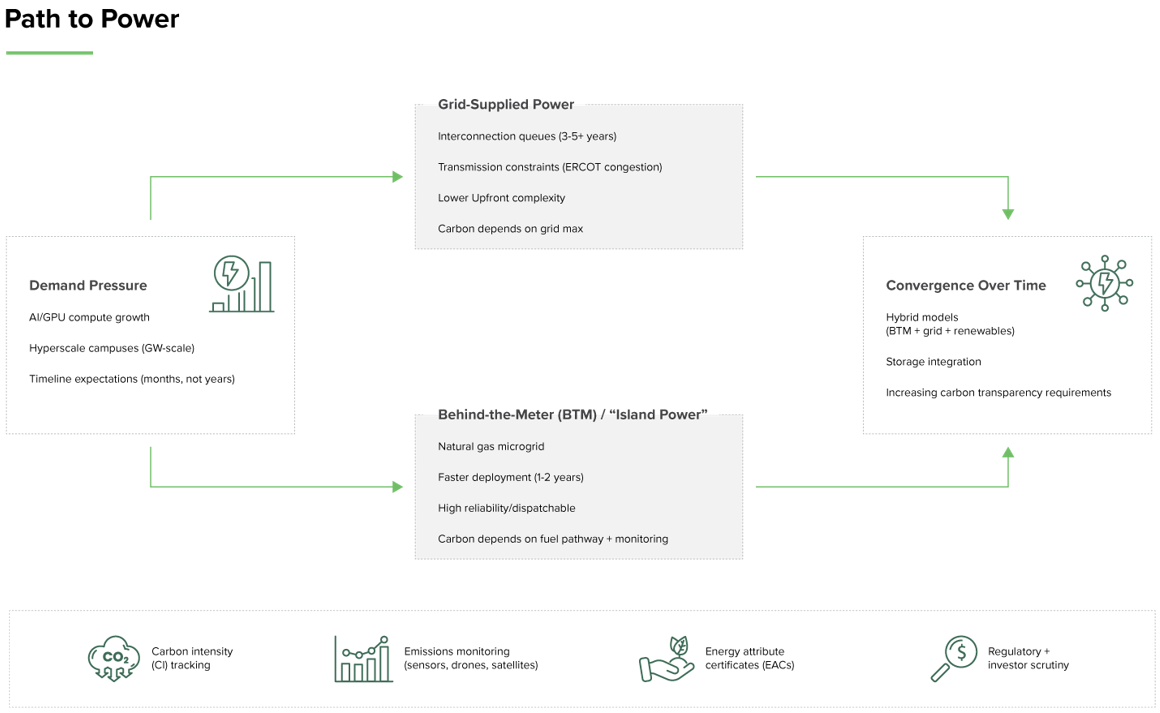

The rapid expansion of artificial intelligence is driving unprecedented electricity demand, with data centers (DCs) emerging as major consumers. Modern GPU-driven models require enormous amounts of power, creating urgent challenges for developers seeking reliable, scalable energy. Estimates from the International Energy Agency (IEA) project that “electricity demand from data centres worldwide is set to more than double by 2030” and the Electric Power Research Institute (EPRI) reports that data centers could account for roughly 9-17% of U.S. electricity demand by 2030. Texas has emerged as a leading market, with major projects like Stargate in Abilene and a collaboration between Oracle and VoltaGrid in the Dallas and Houston areas.

According to ERCOT’s long-term load forecast, peak demand in Texas could nearly double by 2030. Some industry estimates suggest hyperscale campuses could require multiple gigawatts of capacity, potentially equivalent to more than 1 Bcf/d of natural gas demand. Transmission infrastructure is stressed, and interconnection timelines can extend five years or more, according to analysis by the Federal Energy Regulatory Commission (FERC). AI providers and investors expect facilities to be online much sooner.

To address grid bottlenecks and reduce time-to-power, developers are increasingly exploring behind-the-meter (BTM) natural-gas-fueled microgrids (“Island Power”) that can provide reliable power while grid infrastructure catches up.

The choice between grid-supplied power and behind-the-meter generation is becoming a defining strategic decision for developers.

With power availability coming into focus, the carbon profile of that energy is becoming the next critical consideration.

Carbon Intensity: The New Competitive Edge

Microsoft, Meta, Alphabet, AES and others are increasingly focused on the carbon intensity (CI) of compute produced at data centers. These companies have large carbon accounting departments and ambitious net-zero targets, making CI a critical factor in long-term compute buyer leases and commercial energy acquisition.

In the near term, many developers view natural gas as a necessary complement to renewables, helping meet intermediate power generation needs. While natural gas combustion produces lower emissions than many alternatives, methane leakage across the fuel pathway remains an important contributor to overall carbon intensity. (Methane traps far more heat than CO₂ — about 80 times more over 20 years — so leaks during production or transport greatly increase climate impact.)

Producers, pipeline operators and other NG pathway participants can impact segment CI through investment and operational practices. Recognizing CI by a pathway segment enables compute buyers to identify the lowest CI alternatives, thereby reducing carbon offset purchase obligations. As carbon intensity becomes a commercial consideration, the ability to measure and verify emissions is becoming equally important.

CI Monitoring and Reporting

Across the value chain, emissions monitoring is evolving from estimates to measured data. Advances in monitoring technology have improved the way emissions across the natural gas supply chain are measured, verified and reported. Driven by technology, policy and the demands of gas operators trying to differentiate their product, actuals are replacing estimates.

Onsite emissions monitoring: Data center operators and natural gas producers are deploying real-time, onsite sensors to measure and report greenhouse gas emissions directly at the source. These systems provide granular, continuous data that supports operational improvements and regulatory compliance.

Drone-based emissions surveys: Innovative companies are using drone technology to conduct aerial surveys of facilities and infrastructure. Drones equipped with advanced sensors can detect methane leaks and other emissions across large areas, enabling rapid response and targeted mitigation.

Satellite imaging platforms: Satellite-based monitoring platforms offer global coverage and high-resolution detection of methane and other greenhouse gases. Companies such as GHGSat and Kairos Aerospace provide independent, third-party verification of emissions data, supporting transparency for buyers and regulators.

Academic research and validation: Academic institutions and research labs, including the Energy Emissions Modeling and Data Lab (EEMDL), have been central in providing estimates of natural gas fuel pathway emissions. Today academia is moving beyond modeling historic data to validating real-time monitoring and reporting capabilities. This helps ensure that data center developers and energy buyers have access to credible, science-based emissions data for decision-making and reporting.

Lifecycle Emissions and Voluntary Carbon Accounting

The future of carbon accounting for DCs is likely to be voluntary, especially in Texas. The primary buyers of compute (AI providers) are driving demand for CI data and transparency, and the buildout of DCs will lead to a world where CI data increasingly accompanies commercial energy acquisition.

Lifecycle emissions (Scopes 1, 2, 3) (Definitions follow the Greenhouse Gas Protocol):

- Scope 1: Direct emissions from combustion

- Scope 2: Indirect emissions from purchased electricity

- Scope 3: Upstream methane leakage and supply chain impacts

Energy Attribute Certificates and Evidence of Carbon Intensity

Energy attribute certificates (EACs) allow energy buyers to replace estimated emissions factors with more precise measurements of actual emissions performance. EACs are increasingly available for NG fuel pathway segments, providing evidence of CI.

Carbon accounting “standards” will need to accept the EAC methodology, but that will happen over time. In the meantime, a limited assurance opinion will help the EAC owner employ it as part of their accounting process. Data center operators can select lower-CI natural gas supply chains with the lowest CI to support long-term compute buyer leases.

Types of NG in the fuel pathway:

Traditional NG (fossil): The standard supply, with CI determined by methane leakage and operational practices.

Renewable NG: Produced by capturing methane from landfills, manure and wastewater. Supported through government incentive programs, then commingled with fossil NG and limited in supply.

Differentiated gas: EACs give energy buyers tools to score and report their fuel-buying choices. Differentiating natural gas based on carbon intensity could encourage innovation across the fuel pathway while helping ensure reliable energy supplies for AI infrastructure.

Integrating Energy Strategy, Carbon Transparency and Market Risk

As data center developers respond to accelerating power demand and increasing scrutiny around carbon intensity, many are seeking integrated advisory capabilities that address both energy strategy and commercial risk.

This includes evaluating behind-the-meter power options, structuring energy procurement and hedging strategies, and implementing carbon accounting frameworks that can withstand investor and regulatory scrutiny.

Weaver supports these efforts through carbon accounting, sustainability strategy and emissions reporting, helping organizations quantify lifecycle emissions (Scopes 1, 2 and 3), validate carbon intensity claims and implement transparent reporting frameworks.

95delta brings complementary capabilities in energy trading, commodity risk management and valuation of physical and derivative portfolios, supporting clients in structuring PPAs, managing fuel price exposure and navigating carbon market risk.

Together, these capabilities help data center developers and operators align energy procurement, carbon strategy and risk management as they scale infrastructure in a rapidly evolving market. For information or assistance, contact us.

Authored by Ashly Pleasant, Holly Roozrokh and 95delta

©2026