The Tax Impact of Dealer vs. Investor Status in Real Estate

Never miss a thing.

Sign up to receive our Tax News Brief newsletter.

Minimizing future tax liability in real estate starts long before the sale — it begins with strategic planning early in the investment life cycle. For example, the distinction between dealer versus investor can significantly impact a taxpayer’s bottom line. This classification determines whether gains are taxed at capital gains rates or as ordinary income — a substantial difference in tax liability. This is important as tax treatment directly correlates to the intention of the entity’s real estate investment plan on a property-by-property basis. Given that a property’s classification can change during the ownership period, proactive planning is essential to defend against potential IRS challenges during subsequent tax years.

Understanding the Dealer vs. Investor Tax Distinction

This leads us to the overarching question of dealer versus investor classification for tax purposes. This distinction determines whether gains and losses should be classified as capital (taxed as high as 23.8%) or ordinary (taxed as high as 40.8%) and is heavily dependent on investment intent. When determining whether you or your client is a dealer or investor, it is crucial to ensure you meet as many criteria as possible for either classification, as the courts could reclassify gain/loss between capital and ordinary, with the potential to tack on additional tax. Additionally, investors are eligible to report under installment sales, while dealers are not (IRC Sec 453(b)(2)).

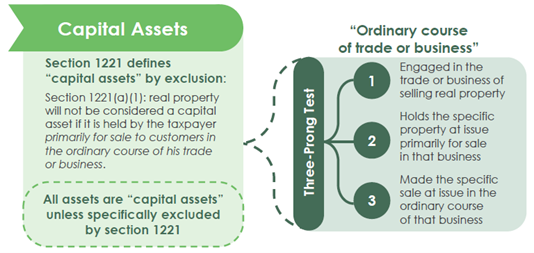

In short, a taxpayer that meets the definition of an investor is allowed capital gain/loss treatment, while a dealer uses ordinary income/loss treatment. With capital gain/loss treatment being more advantageous from a taxation perspective, it is important for the taxpayer to meet certain criteria in order to access the lower tax rates associated with the sale of capital assets or investments. First off, you will need to determine if the assets sold are indeed capital assets by definition per IRC section 1221.

Key IRS Factors Affecting Real Estate Tax Status

When determining whether a taxpayer is a dealer or investor, it is based on facts and circumstances, as no two situations are the same. However, various court cases lay out factors that are important to consider. The most notable being U.S. v. Winthrop, which led to a seven-factor test for determining classification. These factors include:

- Nature and purpose of the acquisition of the property and duration of ownership

- Intent when purchasing and holding real estate is vital in determining dealer or investor status, however this can change over the holding period. For example, in Sugar Land Ranch v. Comm., the taxpayer intended to develop property and ultimately was unable to secure funding in order to develop. Because of this, investor status was upheld by the tax court, contrary to the IRS classification of a dealer based on original intent. This burden of proof is heavy when converting from dealer to investor.

- Extent and nature of the taxpayer’s efforts to sell the property

- If the taxpayer makes substantial efforts to market and sell the property (including using brokers, agents and advertising), courts have historically ruled that this leans toward ordinary/dealer treatment.

- Frequency and continuity of sales

- If sales of real estate are frequent and continuous, this may indicate an ordinary trade or business by a dealer. Alternatively, if sales are infrequent and for larger profits, this may point towards an investment as outlined in Suburban Realty Co. v. U.S. and Phelan v. Commissioner.

- Nature and extent of improvements, subdivision and advertising to increase sales

- If the taxpayer is engaging in activities such as building utility infrastructure, grading and zoning these would point to dealers, as they are engaged in the trade of real estate. In short, if the taxpayer is putting shovels into the ground, they would be considered a dealer/developer.

- Use of a business office for the sale of property

- If the taxpayer maintains an office used to dispose of the property and/or holds licenses and permits to sell the property, courts have ruled for ordinary treatment.

- Degree of supervision/control exercised by the taxpayer over any representative selling the property

- This factor is highly dependent on facts and circumstances, and extent is key. In some cases, the use of an agent supported capital gains treatment, while others met capital treatment without the use of an agent.

- Time and effort devoted to sales

- Historically, courts have ruled toward ordinary/dealer treatment if substantial amounts of time and effort are involved in sales. This creates the appearance of working with inventory, rather than investments.

Courts have generally placed the highest importance on factors one, three and four.

How to Optimize Tax Planning for Real Estate Sales

Real estate developers should take the dealer or investor status into consideration as this affects the associated tax rates assessed. From a tax compliance/defense perspective, it is important for the taxpayer to best position themselves on one side or the other based on the above points, whether the business is in the process of being established or is already in existence.

Contact a Weaver tax professional to ensure you have the most efficient tax structure possible. We’re here to help.

Authored by Mark Pacinda

©2025