Expanding Supply of Urgent Care Centers Create FMV Considerations

Health Care Valuation Services

Health Care Valuation Services

Never miss a thing.

Sign up to receive our insights newsletter.

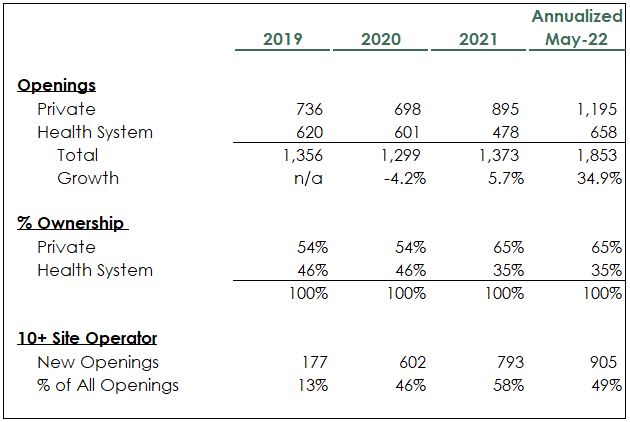

Accelerated Facility Count Growth Illustrates Relative Low Barriers to Entry

Urgent care operators (especially those well capitalized by private equity funds) have invested a record amount of capital to open new (de novo) sites in 2022. This influx of new supply represents the industry’s reaction to significant historical and anticipated patient demand. New center growth is evident in every ownership category, but private national and regional operators with 10+ sites represent the most active category over the last year and a half.

By the Numbers

Source: Weaver Analysis of National UC Realty Data

Based on the information above, we make the following observations:

- The ability for market participants to open so many sites on an annual basis is characteristic of an industry with low barriers to entry.

- There has clearly been a surge of new openings in 2022 as investors take opportunities to capture growing demand, but to a lesser extent, other factors also may be contributing to the increase. These include centers planned for 2021 openings that experienced construction delays during the pandemic.

- Health system openings have remained steady, but they represent a declining percentage of total openings in 2021 and 2022.

- National and regional operators with 10+ sites represented 50% of new openings so far in 2022, up from 13% of new openings in 2019. Growth for this cohort is clearly a function of their access to significant available capital.

- While the data does not capture urgent care closures or relocations, we know this number has been small over the last two years due to pandemic induced patient demand growth.

Yes, But…

- Those opening new sites, especially large operators, are betting accelerated patient demand for urgent care will continue beyond the foreseeable future. If actual demand is less than expected, the growth in new urgent care sites will be (in retrospect) an over-reaction and could cause an over-supply situation.

- The acceleration of new openings may increase competition for qualified health care workers, exacerbating existing shortages and rising labor costs. Combined with continued supply inflation, new (as well as existing) sites may need to achieve higher patient volumes than previous to maintain profitability levels.

Health Care Valuation Takeaways

- New center growth is clearly a vote of confidence in the industry as a whole, as evidenced by the significant investment in capital and management resources to grow site count.

- Valuators need to address the impact of new competition due to low barriers to entry. Successful urgent care centers may be tested, especially if patient visit volume declines within the respective market.

- The valuator needs to weigh a subject urgent care center’s merits along with its exposure to potential or new competition.

Dig Deeper

For information about health care provider valuations, contact us. We are here to help.

© 2022

This is one in a series of related health care valuation posts:

- Surgery Outmigration Driving Elevated Valuation Multiples in the ASC Segment

- Increased Contract Labor Costs May Lead to Valuation Revisions

- Revenue Growth and EBITDA Multiple Expansion Drove Historical Health Care Investment Returns

- Behavioral Telehealth Growth May Mean Opportunities for Inpatient Operators

- The Future of US Health Care Profits

- Hospital Expense Statistics Illustrate Significant Labor Pressures

- Hospital Earnings Supported by Fewer Uninsured Patients

- Health Care Services Transaction Volume Declines Below Pre-Pandemic Levels