The Importance of a Stable Payer Mix to a Premium Valuation

Article

4 minute read

June 11, 2021

The Implied Valuation Risk of Long Term Payer Mix Shifts

Health care providers face future revenue challenges as patient payer categories gradually shift from Commercial Payers to Government Payers. The valuation implications of lower future average pricing can be significant, but largely depends on the starting point. If the subject company enjoys a high relative Commercial Payer mix, future pricing diminution will be more drastic as the payer mix shifts toward Government Payers.

The Big Picture

- The reasons for the payer shift are complex, but have their roots in demographics and the aging of the population. In 2014, Government Payers represented 44.7% of the hospital payer mix. Since then, Government Payers increased their share of the pie by approximately 0.5% annually to 46.8% by the end of 2018 (Source: Moody’s). At this rate, Government Payers will (conservatively) represent ~52.0% of the hospital payer mix by 2028.

- Some providers have “more to lose” as payer relationships and local market power yield much higher than average commercial payments.

- Higher relative commercial payment rates equate to a higher risk of significant profit diminution as the payer mix shifts.

- Typically, commercial payment rates are determined through negotiations with insurance companies, and can vary depending on market conditions, such as the bargaining power of individual providers relative to insurers in a community.

By the Numbers

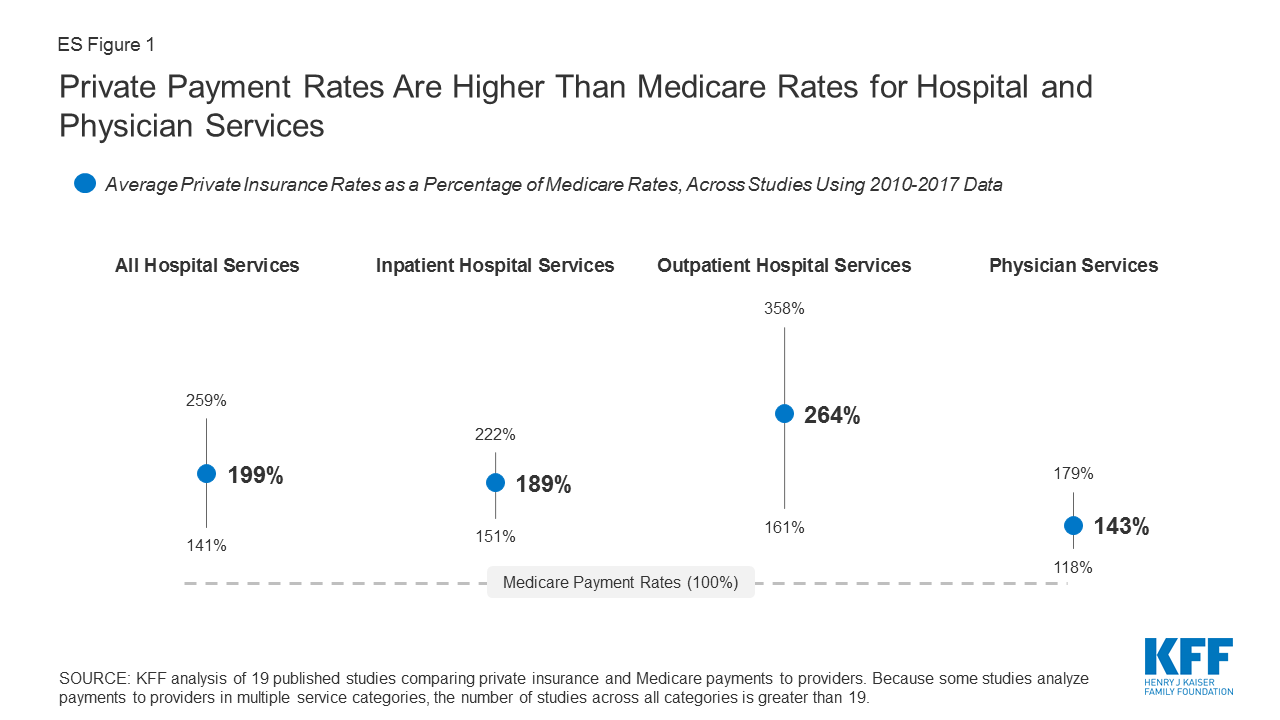

In a report issued April 15, 2020, The Kaiser Family Foundation reviewed the findings of 19 recent studies comparing Medicare and private health insurance payment rates for hospital care and physician services.

Among the findings:

- On average, commercial premium payments (i.e. commercial payment rates to facility operators as a percentage of the Medicare payment rate for the same service) exceed Medicare by 189% for inpatient services and 264% for outpatient services, and 143% for physician services.

- The variability of commercial premiums was greater for outpatient services (200% spread) than for inpatient services (70% spread). The wide variability suggests that, even within a given health care market, some individual providers are outliers in that they can command extremely high private reimbursements.

- Measuring the commercial premium is complex and inexact. The studies KFF analyzed may omit unique payment characteristics and features such as Medicare supplementary payments, risk-based contracts, and may include or exclude commercial out of network payments.

Health Care Valuation Takeaways

- Health care valuators should understand the subject company’s exposure to possible payer mix shifts and the related implications on future profits.

- Health care valuators should analyze the size of the subject company’s commercial premium along with the speed and magnitude of the shifts. Importantly, they should assess management’s long-term strategic plans to alter the structure of the business to mitigate these trends in order to operate successfully under a new payment environment.

- With the high variability of the average commercial premium, the subject company could be significantly higher than the average and therefore may be at risk for accelerated payment rate diminution. To maintain and support a valuation premium, the valuator should ensure the payer mix is steady and displays durability for future time periods.

- Due to the shift to Government Payers, applying general market multiples to current profit metrics may not sufficiently capture the risk of payment rate declines specific to the subject entity. This is especially true if the current commercial premium is above the averages identified in the KFF study.

Go Deeper

© 2021

This is one in a series of related health care valuation posts:

- Urgent Care Centers Embrace a Once in a Generation Business Opportunity

- Closing the Gap Between Perceived and Actual Demand in Behavioral Health

- After the Pandemic, What Are the Long-Term Valuation Implications for Long Term Acute Care Hospitals?

- Hospice Valuations in a High Multiple Comparable Sales Environment

- Guarding the Shelf Life of Fair Market Value Opinions for Management Services Organizations

- Managed Care Companies Predicting the “Worst of Two Worlds”

- Navigating Health Care Valuation EBITDA Multiple Ranges for Fair Market Value

- Navigating Urgent Care Valuations in Unusual Times

- ASC Partnerships Face Succession Challenges